If you want to improve your rental property cash flow, focus on three areas: rental strategy, insurance costs, and property taxes. These changes can add hundreds or thousands of dollars per month to your bottom line, which also improves your debt service coverage ratio (DSCR) and helps you qualify for better financing terms on current and future rentals.

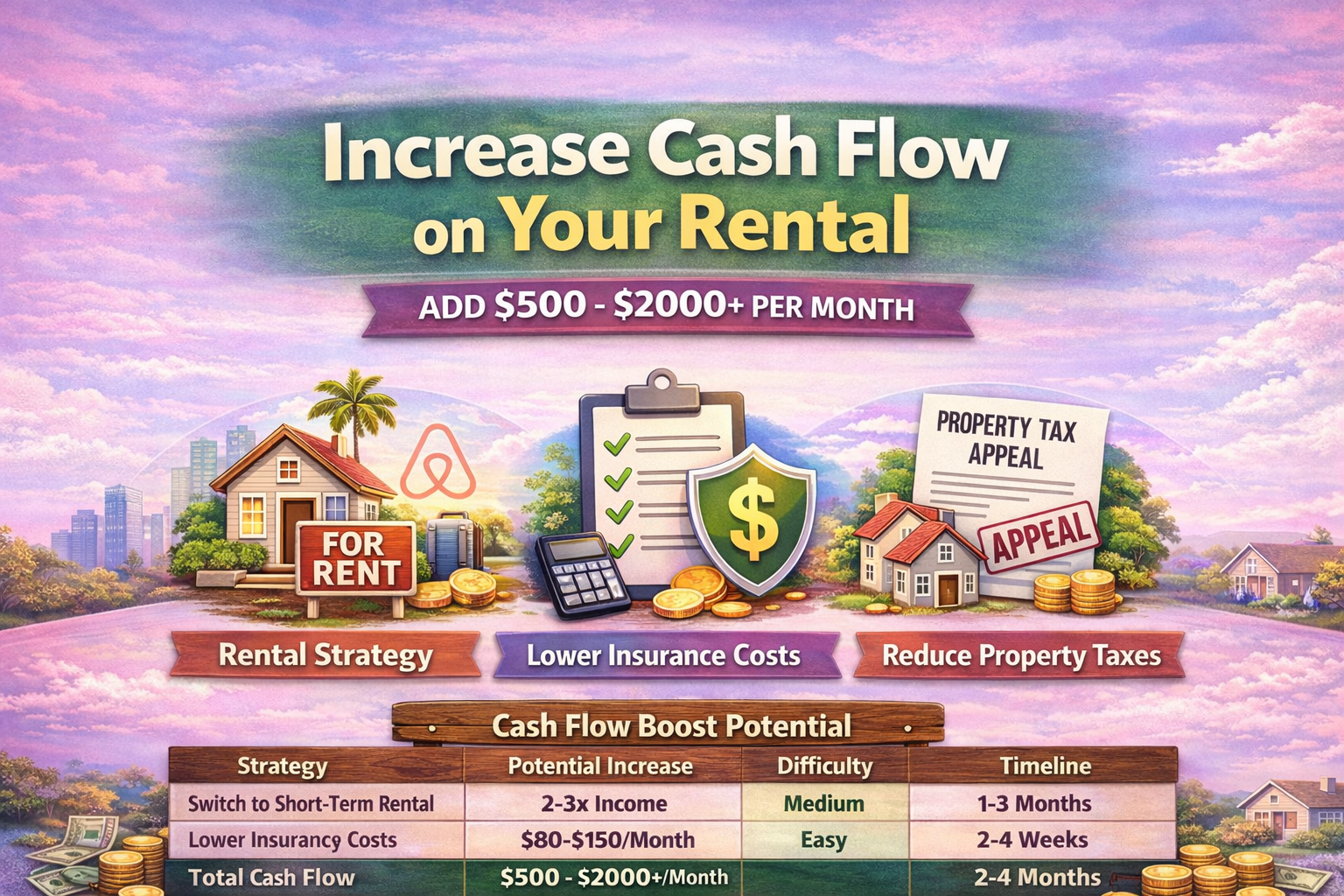

Cash Flow Improvement Comparison Table

| Strategy | Potential Impact | Difficulty | Timeline |

| Switch rental strategy | 2-3x income increase | Medium | 1-3 months |

| Lower insurance costs | $80-$150/month savings | Easy | 2-3 weeks |

| Reduce property tax | $100-$220/month savings | Easy | 2-8 weeks |

| Combined effect | $500-$2,000+ monthly increase | Medium | 2-4 months |

How to Increase Your Rental Cash Flow: Step-by-Step

Step 1: Evaluate Your Current Rental Strategy

Calculate your current monthly income per property. Then research what similar properties earn using alternative strategies like short-term rentals, co-living, corporate housing, or Section 8.

Example: A traditional long-term rental bringing in $1,500 per month might generate $3,000 to $4,500 as a short-term rental in the same market.

Step 2: Shop Your Insurance

Contact at least three insurance providers and request quotes for the same coverage you currently have. Ask about discounts for multiple properties, higher deductibles, or bundling policies.

What to request:

- Landlord insurance quotes

- Liability coverage amounts

- Deductible options

- Multi-property discounts

Step 3: Appeal Your Property Taxes

Use a property tax reduction service like Ownwell. These companies review your property assessment, file appeals if you are overassessed, and only charge you if they successfully lower your taxes.

How it works:

- Sign up with the service

- They review your current assessment

- They file the appeal on your behalf

- You only pay if they win

Deep Dive: Understanding Each Strategy

Alternative Rental Strategies Explained

Short-term rentals are properties rented by the night or week, typically through platforms like Airbnb or VRBO. They require more management but generate significantly higher income in tourist areas or business districts.

Co-living involves renting individual rooms in a single property to multiple tenants. A four-bedroom house might rent for $1,800 as a whole unit but generate $2,800 when rooms are rented separately at $700 each.

Corporate housing targets business travelers or relocated employees who need furnished, month-to-month rentals. These tenants pay premium rates for flexibility and convenience.

Section 8 is a government housing assistance program. Landlords receive guaranteed rent payments directly from the housing authority, often at market rate or above, with less turnover than traditional rentals.

How Insurance Shopping Works

Insurance companies use different risk models and pricing. The same property with identical coverage can vary by $500 to $2,000 annually between providers.

What affects your insurance rate:

- Claims history

- Property age and condition

- Location and crime rates

- Deductible amount

- Coverage limits

- Number of properties insured

Shopping every 12 to 24 months keeps your rates competitive.

Property Tax Appeals Process

Property assessments are not always accurate. Assessors may use outdated comparables, incorrect property data, or overestimate your property value.

Common reasons for successful appeals:

- Assessment higher than recent sale price

- Assessment higher than comparable properties

- Incorrect property information (wrong square footage, bedroom count)

- Market decline since last assessment

Services like Ownwell handle the entire process. They typically charge around 25% of your actual tax savings.

Common Mistakes and How to Avoid Them

Mistake 1: Not Running the Numbers Before Switching Strategies

Do not assume short-term rentals work everywhere. Research occupancy rates, average daily rates, and operating costs in your specific market before making the switch.

How to avoid: Use tools like AirDNA or analyze actual listings in your area before deciding.

Mistake 2: Accepting the First Insurance Quote

Many investors renew their insurance automatically without comparing rates. This costs thousands over time.

How to avoid: Set a calendar reminder every 18 months to request three competitive quotes.

Mistake 3: Ignoring Property Tax Assessments

Property owners often receive their tax bill and pay it without reviewing the assessment for accuracy.

How to avoid: Review your property tax assessment every year when you receive it. Compare it to recent sales of similar properties in your neighborhood.

FAQ: Rental Property Cash Flow

How much can I realistically increase my cash flow?

It depends on your market and current strategy. Investors who switch from long-term to short-term rentals typically see 1.5x to 3x income increases. Insurance and tax reductions usually add $100 to $300 monthly per property.

Do I need special permits for short-term rentals?

Most cities require short-term rental permits or licenses. Research your local regulations before converting a property. Some cities have strict limits or outright bans.

How often should I shop for insurance?

Every 18 to 24 months. Your risk profile and the insurance market both change over time.

Will appealing my property taxes hurt me later?

No. Property tax appeals are a normal part of property ownership. Successful appeals do not trigger audits or negative consequences.

What DSCR do most lenders require?

Most portfolio lenders want 1.00 minimum. Better cash flow, such as 1.20 or higher, often qualifies you for lower interest rates and higher leverage.

Can I switch back if short-term rentals do not work?

Yes. You can always return to traditional long-term rentals. Test short-term rentals for 6 to 12 months before making permanent decisions.

Do these strategies work for properties I am buying with financing?

Yes. In fact, they work better. Higher cash flow improves your DSCR, which helps you qualify for financing and potentially secure better terms.

How long does a property tax appeal take?

Usually 14 days to 60 days depending on your county and whether your case goes to a hearing.

What if I have multiple properties?

Apply all three strategies across your portfolio. Even small improvements on multiple properties add significant monthly income.

Should I do all three at once?

You can, but prioritize based on impact. Start with rental strategy research, then shop insurance while waiting, then file tax appeals.

Glossary of Terms

DSCR (Debt Service Coverage Ratio)

A calculation lenders use to measure cash flow. Divide your monthly rental income by your monthly PITI, which includes principal, interest, tax, insurance, and HOA if applicable. A DSCR of 1.25 means you earn $125 for every $100 of monthly payments. Most lenders want a minimum of 1.00.

ARV (After Repair Value)

The estimated value of a property after renovations are complete.

LTV (Loan-to-Value)

The loan amount divided by the property value, expressed as a percentage.

Short-term rental

A property rented for less than 30 days at a time, typically through platforms like Airbnb or VRBO.

Co-living

A rental strategy where individual rooms are rented separately within a single property.

Property tax assessment

The value assigned to your property by the county assessor, used to calculate your property taxes.

Occupancy rate

The percentage of time a rental property has paying tenants.

Take the Next Step

If you are actively working on improving cash flow on your rental properties and want to discuss how better numbers affect your financing options, I am happy to walk through your numbers. Understanding your cash flow helps me structure better lending terms for your next acquisition or current cash out refinancing.

Schedule a time on my calendar today and we can review your current portfolio and your next deal together.

About the Author

Dahae Yi is a commercial mortgage lender and real estate funding educator specializing in fix & flip and BRRRR financing. She teaches investors how to structure lender-ready deals and offers flexible, relationship-based funding terms that improve as the partnership grows. Her content is designed to help investors scale faster, avoid common funding mistakes, and make the funding process easy.

Follow her on Instagram: @dahaeyi.lender

Leave a Reply